The more pessimistic analysts believe that UK house prices could drop by as much as 30% over the next couple of years. Property prices leapt alongside most other asset classes over the long bull market that ran relatively uninterrupted over the 13 year period from the start of the recovery from the international financial crisis in 2009 and last year.

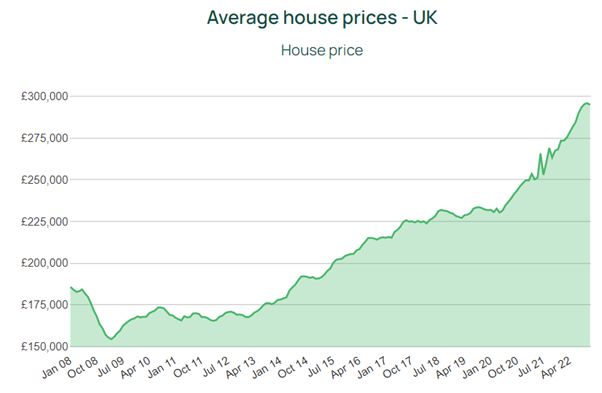

Average prices across the country almost doubled from £154,500 in March 2009 to just under £296,000 in October last year, when the market hit its most recent record high. Global stock markets had been in a downward spiral for almost a year while property prices kept climbing.

Source: PropertyData

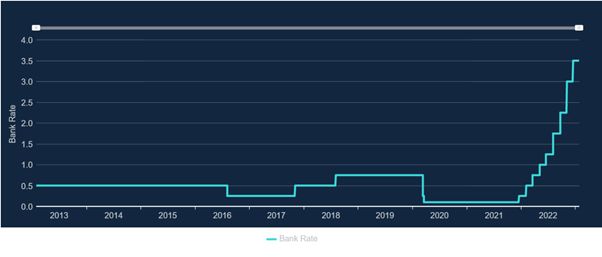

However, a combination of rising interest rates, up from 0.1% in late 2021 to 3.5% in January 2023 and further hikes expected this year, soaring inflation putting pressure on household budgets and nerves around a recession has seen house prices ease. There still not far off their record highs of late 2022 but the trend is downward.

Source: BankofEngland

The big question for homeowners and property investors is just how far could UK residential property prices drop over the next couple of years? How long prices might take to recover from a drop is another important unknown.

First time buyers struggling to get onto the property ladder may welcome a significant drop in UK house prices. Even if higher interest rates mean monthly mortgage costs don’t change much, lower sales prices should reduce the minimum deposits required to secure a mortgage.

However, for anyone who currently owns a home, especially if purchased in the past couple of years towards the top of the market, a significant drop in valuation would be extremely unwelcome. That is particularly the case for home owners at risk of falling into negative equity, which means the market value of their property is lower than the outstanding sum due on the mortgage.

Falling house prices, if the decline is steep, could also create a wider economic crisis and spill over into other parts of the economy and financial markets.

But not everyone agrees UK house prices will drop by anywhere near 30%. Let’s explore the factors that would affect the residential property market over 2023 and beyond and different opinions on how serious a market slump could be. As well as the wider potential consequences that could result if the dive in home valuations turns out to be in line with more negative forecasts.

How much will UK house prices fall by?

The short answer to that question is that we don’t know but the most pessimistic outlook is for drops of up to 30% over the next couple of years. However, there are a number of factors that mean there is a high chance valuations will slide by less. But let’s look at the negative scenario first.

A 30% drop in home valuations sounds like a lot and it is. However, against the backdrop of the last couple of years that kind of fall looks a little less extreme. Prices are up 28% since April 2019 and a 30% fall would take the average price of a home in the UK to around £210,000, where it was in 2016. A less severe 20% drop in prices would see the average price settle at around £235,000, where it was just before the onset of the Covid-19 pandemic and the Bank of England dropping interest rates to just 0.1%.

Mid-term interest rates are likely to have the biggest influence on house prices. At the BoE’s current 3.5% base rate, the best mortgage deals available are 2 years fixed at 4.8% compared to 1% deals available until recently. At an LTV of 60% on a £400,000 mortgage, that would push the monthly rate up to £2300 a month from £1500 a month.

For some borrowers, that is likely to prove problematic. It is also likely to mean lower demand for properties from buyers who might have otherwise decided to move up the property ladder and first time buyers. A drop in demand at higher price brackets due to affordability thresholds being passed will see property prices fall.

Will demand drop enough to lead to a 30% fall? That depends on factors that are currently unknown. How high interest rates go will have a huge influence and that will depend on inflation. There are signs inflation is easing and today the Fed’s preferred gauge for inflation, the personal consumption expenditures (PCE) price index, rose 5.0% in December from a year earlier. That was slower than the 5.5% 12-month gain as of November and the lowest level since September 2021.

In the UK, inflation has also eased from 11.1% year-on-year in October to 10.5% in December. It’s still much higher than in the USA but will hopefully now maintain a consistent downward trend helped by easing energy prices.

There are hopes the Fed will pull back on further interest rate rises from March and that would set a tone that the Bank of England may well follow with a slight delay. The Fed’s base rate is also already higher than in the UK at 4.25% to 4.5%.

If interest rates and, more importantly, mortgage rates do not rise by more than 1% from where they are today it is unlikely valuation drops of as much as 30% eventuate. But if they did what would the consequences be?

What happens if UK house prices fall 30%?

The good news is that even a house price fall as extreme as 30% would be unlikely to lead to systematic issues in the UK’s financial services sector. More people own their homes outright than have a mortgage – 8.8 million to 6.8 million homes. Lloyds Bank, one of the UK’s biggest mortgage lenders recently reported the average LTV of its mortgage portfolio is just 40%.

Even if average LTV is a little higher for other banks, a wave of defaults is unlikely to threaten their stability and infect other areas of financial markets or the wider economy. Mortgage lenders are also reluctant to repossess homes they’ve lent against as it’s an expensive process for them. They will do as much as they can to work with borrowers who are struggling to meet increased mortgage payments.

What does falling property prices mean for investors?

For property investors, it’s really a case of if rental income will continue to cover mortgage payments, or get close enough to mean the investment still adds up. If mortgage payments are likely to exceed realistic rental income over the next few years investors may consider selling up. Unless the property was purchased in the last 2-3 years, that could still mean walking away with a reasonable return.

For investors in the wider financial markets, it seems unlikely that falling property prices, even if up to 30% is knocked off valuations, will see serious contagion spread and spark a crisis.

It’s not impossible that UK property prices could fall by as much as 30% over the next couple of years as a result of higher interest rates and tighter household budgets but the likelihood is the average drop will be less. And in the worst case scenario, wider fallout should be limited. A repeat of the systemic crash that led to the 2008 financial crisis does not seem like a real prospect. Lenders are well capitalised and the system looks strong enough to cope.